2016年7月24日星期日

24 Key Numbers Investors Should Know About Parkway Life REIT

Parkway Life REIT (SGX: C2PU) is one of the many companies and real estate investment trusts (REITs) in Singapore’s stock market that have released their annual reports over the past few months.

The annual report is a great place to learn more about a company or trust. In the case of Parkway Life REIT, its latest 2015 Annual Report had a chockful of interesting numbers. Here are 24 figures that may be worth noting:

At the end of 2015, Parkway Life REIT had a total of 47 properties across Singapore, Japan, and Malaysia. The portfolio was valued at around S$1.6 billion as at 31 December 2015, placing the REIT as one of the largest healthcare REITs in the region.

Singapore accounted for 63% of gross revenue in 2015, followed by Japan at 36.5%. The remainder came from Malaysia.

Parkway Life REIT’s distribution per unit (DPU) was 13.29 Singapore cents in 2015. This is an 86.6% jump from its initial annualised DPU of 6.32 cents seen in 2007. The accumulated DPU from the REIT’s IPO (initial public offering) up till the fourth-quarter of 2015 is 81.1 cents. Parkway Life REIT’s IPO price was $1.28 per unit.

Parkway Life REIT entered the Japan market in 2008. Since then, it has been able to build up a portfolio of 43 healthcare properties in Japan that are worth a total of S$590 million.

During the year, Parkway Life REIT acquired seven new Japanese nursing homes. This allowed the REIT to make its first foray into the Aichi Prefecture in Japan. This followed its maiden divestment made in late 2014, when seven other Japan nursing homes were sold off for a profit of $9.11 million.

Parkway Life REIT has a fairly healthy debt profile. The REIT has a weighted average term to loan maturity of 3.5 years and a gearing of around 35.3% at the end of 2015. There is no year in which more than 32% of its total debt will come due.

On Parkway Life REIT’s leases, 64% of its gross revenue has a CPI-linked revision formulae. Furthermore, 98% of its leases (by nett lettable area) comes with a rent review provision. At the end of 2015, Parkway Life REIT had a weighted average lease term to expiry of 9.12 years. Only 2.5% of its leases will expire between 2016 and 2020.

Parkway Life REIT also presented some stats on the healthcare sector. The global population aged 60 and above will rise to almost 22% by 2050, up from 12.3% today. Closer to home, the number of Singaporeans aged 65 and above has doubled to 440,000 in 2015 over the past 15 years. This is expected to more than double to 900,000 by 2030. As a result, Singapore’s healthcare spending is expected to reach more than S$13 billion in 2020.

There could be competition for medical tourism. The medical tourism market in Malaysia has nearly doubled since 2010. Meanwhile, revenue growth for Thailand’s hospitals was up to 15% year-on-year. Singapore, though, remains popular for high-end treatment.

我買日本 Reits的原因

1) 分散地域風險,亞太區雖是增長最好的地方,個別地區,不同sector表現仍有很大分別!如新加坡及香港酒店業表現向下,日本澳洲則較佳。

2) 日本旅遊業增長勢頭甚佳,預料海外遊客會由現時2000萬增長至2020年奧運會的4000萬!但酒店的增長數目緩慢,入住率不斷攀升。

2) 日本旅遊業增長勢頭甚佳,預料海外遊客會由現時2000萬增長至2020年奧運會的4000萬!但酒店的增長數目緩慢,入住率不斷攀升。

3) Office辦公室的表演也不錯,使用率長期穩定地維持在較高水平。空置率預料會由現時的4%跌至2017年的3%,Office workers的數目在主要商業地區如東京、神奈川県、千葉縣、埼玉縣等也上升,對辦公室的需求增加。

4)日本reits的息率較低,一般3-4%。惟日本股市前段時間因英國脫歐,日圓急升,股市下跌,提供購入機會。現在reits距離今年高位有10-15%空間。相對香港reits已屢創新高,日本reits值搏率較高。

5)現在掌握的操作平台可方便地以低息1.22-1.5%借入日圓去買日本資產,可以抵消匯率風險,只剩下價格風險!

2016年7月23日星期六

文章‘’12 things Learned from Ascendas Hospitality Trust’s FY2016 AGM‘’的讀後感

文章的作者親身參與Ascendas hospitality Trust(AHT)的股東週年大會,並將所見所聞記下來,對了解這隻reits很有幫助。新加坡的房託基金投資地域不僅限於星加坡,更遍布全世界。AHT 80%的投資在澳洲、日本、中國等地方的酒店。這對分散地域風險很有幫助!這幾年日本的酒店業務增長不俗,增長達23%。值得大家注意!(筆者考慮直接投資日本酒店房託),會後的股東答問也提供了有用訊息,原來新加坡房託不能直接經營業務(operational business),只能有被動收入(passive income),所以AHT另外就另外成立了business trust經營業務和酒店發展。現時只有2間酒店under reit,其餘的9間under business trust.待發展成熟後就轉移到reit那邊。這叫做stapled security.即把2隻不同運作原理的信託‘’釘‘’在一起,以達致最好投資效益!這令筆者不期然拿香港的房託作比較,香港的房託雖然也有十幾年歷史,但發展相對落後很多,無論在經營策略,範圍,投資選擇等都很局限,盼望政府能主動研究引導房託的發展,從新加坡政府學習,在政策及法規上扶助房託業務的發展,使香港整體房託跟上世界潮流,才不辜負世界金融中心這美譽!

以下是該文章:

Hospitality Trust (SGX: Q1P) (A-HTrust) is a stapled group comprising Ascendas Hospitality Real Estate Investment Trust and Ascendas Hospitality Business Trust. The group invests in and manages a portfolio of hospitality properties across Asia Pacific.

The author attended the trust’s most recent AGM to find out more about its prospects in the face of a weakening global economy and flat tourism sector in some countries.

Here are 12 things I learned from Ascendas Hospitality Trust’s FY2016 AGM:

- A-HTrust’s portfolio comprises 11 hotels across seven cities in four countries – Singapore, Australia, China, and Japan. The trust’s entire portfolio is worth $1.5 billion – an increase of 11% year-on-year. Australia accounts for the largest proportion at 41% but the trust’s exposure down under is spread out evenly among six properties. The trust’s largest property, Park Hotel Clarke Quay in Singapore, accounts for 21% of the portfolio.

- A-HTrust’s current yield is 7.55%. The figure is near the trust’s historical low yield in 2015. Its historical high yield is 9.22% in 2013.

- Gross revenue and net property income (NPI) increased in same currency terms but decreased 5.3% and 2.7% respectively in Singapore dollar terms. This was mainly due to a weaker Yen and Australian dollar. Australia accounted for the largest proportion of NPI at 54.5% while Japan saw the largest increase in NPI year-on-year at 13.2%.

- Master leases accounted for 37.5% of NPI. The management revealed it aims to have master leases account for at least 50% of NPI for longer-term stability.

- Distribution per stapled security rose 6.9% year-on-year despite 5% retention of income by the trust. The increase was mainly due to a $2 million contribution from the divestment proceeds of a property – Pullman Cairns International.

- Average occupancy rates, average daily rates and revenue per available room (RevPAR) were all largely flat year-on-year in Australia and China. Only Oakwood Apartments Ariake Tokyo in Japan saw a large increase in RevPAR year-on-year at 23.3%. The rest of the trust’s properties are anchored by master lease agreements.

- A-HTrust’s gearing ratio decreased to 32.7% from 37.2% a year ago. As far as possible, the trust aims to borrow in the local currency where its properties are located to achieve a natural hedge. So for example, Australia accounts for 41% of the portfolio and, accordingly, 42.5% of the trust’s debt is in Australian dollars. To minimize exposure to interest rate volatility, 91.2% of borrowings are at fixed interest rates.

- Australia and Japan are seeing steady growth in international tourist arrivals. Australia saw 6.9 million tourists visit the country in 2015 – an 8% growth from the previous year. Japan saw even better numbers with 19.7 million tourists – a 47% growth from the previous year! International arrivals in Japan are forecasted to reach 40 million in 2020 with the Olympics being held in Tokyo that year. On a side note, one shareholder remarked that he thoroughly enjoyed his stay in one of A-HTrust’s recently refurbished hotels, Hotel Sunroute Osaka Namba, and recommended everyone to give it a try if in Osaka.

- Singapore and Beijing’s international arrivals remain flat. Singapore only saw 1% growth in tourist arrivals in 2015. While the flat tourist numbers will drag the trust’s performance in Singapore, Park Hotel Clarke Quay is anchored by a master lease with a high proportion fixed income paid to the AH-Trust. Beijing’s international arrivals have been falling from 5.2 million in 2011 to 4.2 million in 2015 – one of the reasons being the city’s bad air pollution. However, China’s domestic travel remains robust; 269 million domestic travelers visited their country’s capital in 2015 which has been growing at 7% per annum since 2011.

- A-HTrust has partnered with NASDAQ-listed Chinese hotel operator Huazhu Hotels Group to operate the trust’s Beijing hotels and tap on their local experience and knowledge in the Chinese market. Huazhu manages/operates over 2,700 hotels in 352 cities in China and has over 49 million members in its loyalty programme. CEO Tan Juay Hiang mentioned that Ibis Beijing Sanyuan has gotten good traction from Huazhu’s loyalty programme and is expecting good results from the partnership moving forward.

- In November 2015, A-HTrust announced that it received an expression of interest from an undisclosed party to acquire the entire trust. The management hired appointed a slew of advisors – JP Morgan, Wong Partnership, KPMG Corporate Finance, and Ernst & Young – to provide financial, legal and tax advice on the viability of the proposal. In the end, the board decided not to proceed with the transaction because they believed it was not in the best interests of shareholders. One well-known local activist investor was not impressed and questioned why so many high-powered advisors were needed to consider a non-binding expression of interest and which party bore the cost of the advisors. The CEO replied that the cost was borne by the trust. Another shareholder pressed to know the total costs involved and the CEO revealed that it was the region of $600,000. A number of shareholders then voiced their displeasure with the board that so much money was wasted for an exercise that eventually amounted to nothing.

- Our activist investor asked why the trust decided to structure itself as a stapled security: a REIT and a business trust. He pointed out that there are tax benefits for REITs – when a REIT pays out at least 90% of distributable income to unitholders – and questioned why A-HTrust would place only two hotels under its REIT and the other nine hotels under its business trust. He carried on to say that most stapled securities use a business trust to undertake property developments (where REITs have a limitation), after which they move the property to the REIT to be more tax efficient. The CEO replied A-HTrust has a stapled structure because a REIT in Singapore is only allowed to earn passive income (rent) and is not allowed to have an operational business. For A-HTrust, some of its hotels are not under a master lease and run on management contracts instead – and therefore can’t be placed under the REIT. In other words, the trust operationally runs the hotel business for some of its hotels. The CEO continued and said that while running a hotel operation means taking on more business risk compared to a master lease, there is also an upside when demand and room rates increase.

2016年7月15日星期五

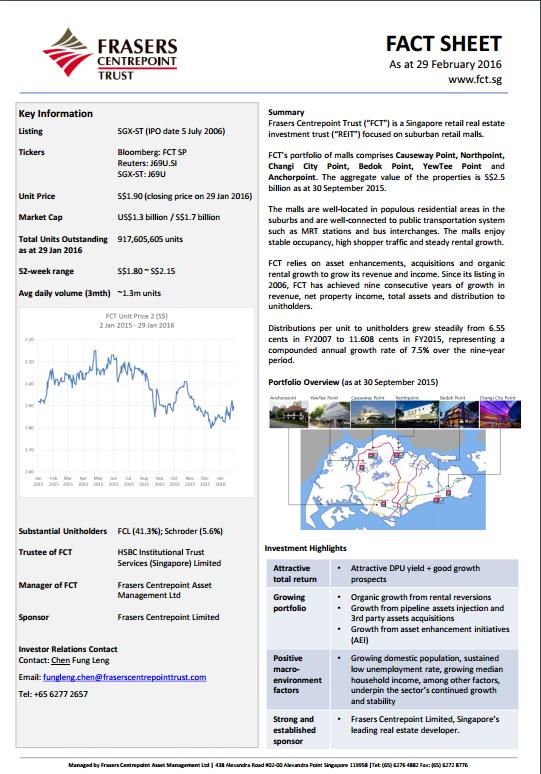

Frasers Centrepoint Trust最新派息及歷年紀錄

FCT剛公佈2016年第3季派SGD$3.04cents,符合預期。收入雖因商場裝修及個別小商場occupation rate下降而減少,派息卻略有增加。下圖表可以看到

歷年派息紀錄非常穩定上升,這是因為組合中多是民生商場有關,經得起經濟週期。買reits除了買回報率,還要揀可以長時間派息穩定上揚。

2016年7月14日星期四

投資REITS及債券的槓干融資平台

筆者開始投資香港和星加坡的REITS,也打算將來投資其他地方的REITS,構成一個房地產信託基金的組合,作為我整個投資組合的重要部份。嘗試比較不同的證券公司和銀行,希望找到一個有效率的投資平台,方便入貨,收息和管理。

我一向有用開耀x,輝x的戶口買賣港股。這兩家也有提供環球證券買賣和收息服務。自然首先考慮它們的收費。以星加坡REITS來說,耀X收0.16%(最低20坡元),佣金較平。輝X則收0.28%至0.38%(最低33坡元)。我最後選擇了耀x購入第一批新加坡REITS。結算時驚訝地發覺他們報的匯率和我在yahoo網上得的有很大出入,所以直接和盤房聯絡,要求同時報Bid 和Ask。居然spread有2%之多!忍痛結匯之餘也想想將來可能換馬,一出一入影響很大,所以又去輝x詢問他們的結匯報價,可能輝x是新加坡公司,差價合理很多。總計支出也平過耀x。

這次交了學費也很值得,以前沒有考慮兌換問題,只考慮佣金多少,原來買賣外地證券這個因素也非常重要。耀x不提供星加坡證券margin,輝立有但利息高,兩者都不是槓干融資之選。

我以前買美股時用過一間美國券商,後來無玩美股就差不多忘記了。這家公司全線上操作,香港有辦事處。平台操作多樣化,可塑性超高,但對我來說太複雜,很吃力去搞清楚每一個環節,深怕按錯掣搞錯冇哂D錢。這次我再上去操作平台看看有否作為,居然發覺有以下驚喜:

1)非美股,即港股和星加坡股收0.08%佣金(最低收HK$18或2.5坡元),澳洲日本佣金亦是0.08%,買美國REITS ETF VNQ也是US$1佣金,方便全球佈局。

2)兌換差價非常低,USD/HKD和USD/SGD的差價是小數點後第四個位。每次不論交易多少,劃一收US$2佣金。

3)Almost 所有香港和新加坡REITS margin融資可做到70%,比私銀還要好

4)Margin 融資利率低,借美金坡紙比我用開的私銀還要低

HKD 借$0 - 780,000 2.555% (BM + 2.5% )

$780,000.01 - 7,800,000 2.055% (BM + 2% )

$7,800,000.01 - 780,000,000 1.555% (BM + 1.5%)

2)平台不易操作,雖有中文平台,但翻譯較差,如不熟英文比較難明白。筆者也要花很多時間去掌握。總算初步識落簡單的指示和貨幣兌換,買了些新加坡REITS

3看完menu都不明白,可打電話問,香港客戶服務一般英文對答,冇廣東話,如懂國語,可打去上海問。筆者兩次電話詢問都可以解決到疑難,算是滿意的!

4)始終全線上操作,心有些不踏實,不像在香港去耀x地舖,見到摸到!

其他優點缺點,有待同好一切發掘。筆者分享這次買新加坡REITS經驗,是盼望更多融資收息朋友一起研究,補充個人的盲點。再者,筆者認識很多較年輕朋友,因未達私人銀行開戶資格而沮喪,不能進入債券及REITS融資收息之門,所以希望找到到一個合適平台,讓大家參考,盼望早日達到財務自由!如發現錯誤,或有更好平台,歡迎指教!😂

我一向有用開耀x,輝x的戶口買賣港股。這兩家也有提供環球證券買賣和收息服務。自然首先考慮它們的收費。以星加坡REITS來說,耀X收0.16%(最低20坡元),佣金較平。輝X則收0.28%至0.38%(最低33坡元)。我最後選擇了耀x購入第一批新加坡REITS。結算時驚訝地發覺他們報的匯率和我在yahoo網上得的有很大出入,所以直接和盤房聯絡,要求同時報Bid 和Ask。居然spread有2%之多!忍痛結匯之餘也想想將來可能換馬,一出一入影響很大,所以又去輝x詢問他們的結匯報價,可能輝x是新加坡公司,差價合理很多。總計支出也平過耀x。

這次交了學費也很值得,以前沒有考慮兌換問題,只考慮佣金多少,原來買賣外地證券這個因素也非常重要。耀x不提供星加坡證券margin,輝立有但利息高,兩者都不是槓干融資之選。

我以前買美股時用過一間美國券商,後來無玩美股就差不多忘記了。這家公司全線上操作,香港有辦事處。平台操作多樣化,可塑性超高,但對我來說太複雜,很吃力去搞清楚每一個環節,深怕按錯掣搞錯冇哂D錢。這次我再上去操作平台看看有否作為,居然發覺有以下驚喜:

1)非美股,即港股和星加坡股收0.08%佣金(最低收HK$18或2.5坡元),澳洲日本佣金亦是0.08%,買美國REITS ETF VNQ也是US$1佣金,方便全球佈局。

2)兌換差價非常低,USD/HKD和USD/SGD的差價是小數點後第四個位。每次不論交易多少,劃一收US$2佣金。

3)Almost 所有香港和新加坡REITS margin融資可做到70%,比私銀還要好

4)Margin 融資利率低,借美金坡紙比我用開的私銀還要低

HKD 借$0 - 780,000 2.555% (BM + 2.5% )

$780,000.01 - 7,800,000 2.055% (BM + 2% )

$7,800,000.01 - 780,000,000 1.555% (BM + 1.5%)

SGD 借 $0 -150,000 (1.5% (BM + 1.5% ))

$150,000.01 -1,500,000(1% (BM + 1%))

$1,500,000.01 -150,000,000 ,(0.5% (BM + 0.5%))

USD 借$0 -100,000 --------------1.9% (BM + 1.5% )

$100,000.01 -1,000,000 ----1.4% (BM + 1%)

$1,000,000.01 - 3,000,000--0.9% (BM + 0.5% )

$3,000,000.01 - 200,000,000-----Greater of 0.5% or(BM+ 0.25%)

5)S&P給這證券公司評級是BBB+,展望正面,資產50億美元。評級比香港很多銀行還要高。

6)有不同topic的web-seminar可以幫助你了解操作方法,當中有英文,國語,廣東話

7)海量的資訊提供和各式操作手法,適合好學兼精力無限的投資者!

8)可買賣超過3000隻美國債券,包括國庫債券,投資級及非投資級債券,也有30-90%的融資額。(這方面操作筆者還未懂,需要多點了解,但看到投資潛力很大,畢竟債券市場比股票大)

缺點

1)轉錢入香港銀行自己戶口即時在網上做到。惟存錢入證券戶口則比較麻煩,要親身拿支票或郵寄去公司,而且一定要自己名開的支票。2)平台不易操作,雖有中文平台,但翻譯較差,如不熟英文比較難明白。筆者也要花很多時間去掌握。總算初步識落簡單的指示和貨幣兌換,買了些新加坡REITS

3看完menu都不明白,可打電話問,香港客戶服務一般英文對答,冇廣東話,如懂國語,可打去上海問。筆者兩次電話詢問都可以解決到疑難,算是滿意的!

4)始終全線上操作,心有些不踏實,不像在香港去耀x地舖,見到摸到!

其他優點缺點,有待同好一切發掘。筆者分享這次買新加坡REITS經驗,是盼望更多融資收息朋友一起研究,補充個人的盲點。再者,筆者認識很多較年輕朋友,因未達私人銀行開戶資格而沮喪,不能進入債券及REITS融資收息之門,所以希望找到到一個合適平台,讓大家參考,盼望早日達到財務自由!如發現錯誤,或有更好平台,歡迎指教!😂

2016年7月7日星期四

我的新Reits 組合

經過半年的摸索,終於動手將REITS加入我的投資組合裡。先試探式每隻買入多少,然後再按個別表現調整比重。還好入市時機不太差,暫時錄得+4%回報。REITS在英國公投脫歐後,還有逆市的上升,確是出人意外,這證明現在REITS也成了資金避難所!下一個階段,會考慮加入美國、日本和澳洲的REITS。

買入Frasers Centrepoint Trust (Singapore)

試探式買入新加坡的Frasers Centrepoint Trust@2.1(SGD),小試牛刀。買的原因是所有商場都不是位於市中心,卻在交通便捷的民生區。受經濟週期影響較少。且保持多年派息增長,yield有5.6%,也算不錯。現P/E=11.8,P/B=1.1,借貸率只28%,還有很大空間收購合適商場,提高回報率!

Frasers Centrepoint Trust 公司網站

Frasers Centrepoint Trust 公司網站

訂閱:

文章 (Atom)